Africa holds major gas reserves, but intra-African trade remains limited

Africa holds around 10% of the world’s proven natural gas reserves and could continue producing at current rates for the next seventy years. Yet, only about 3% of this gas ever crosses an African border to reach another African market.

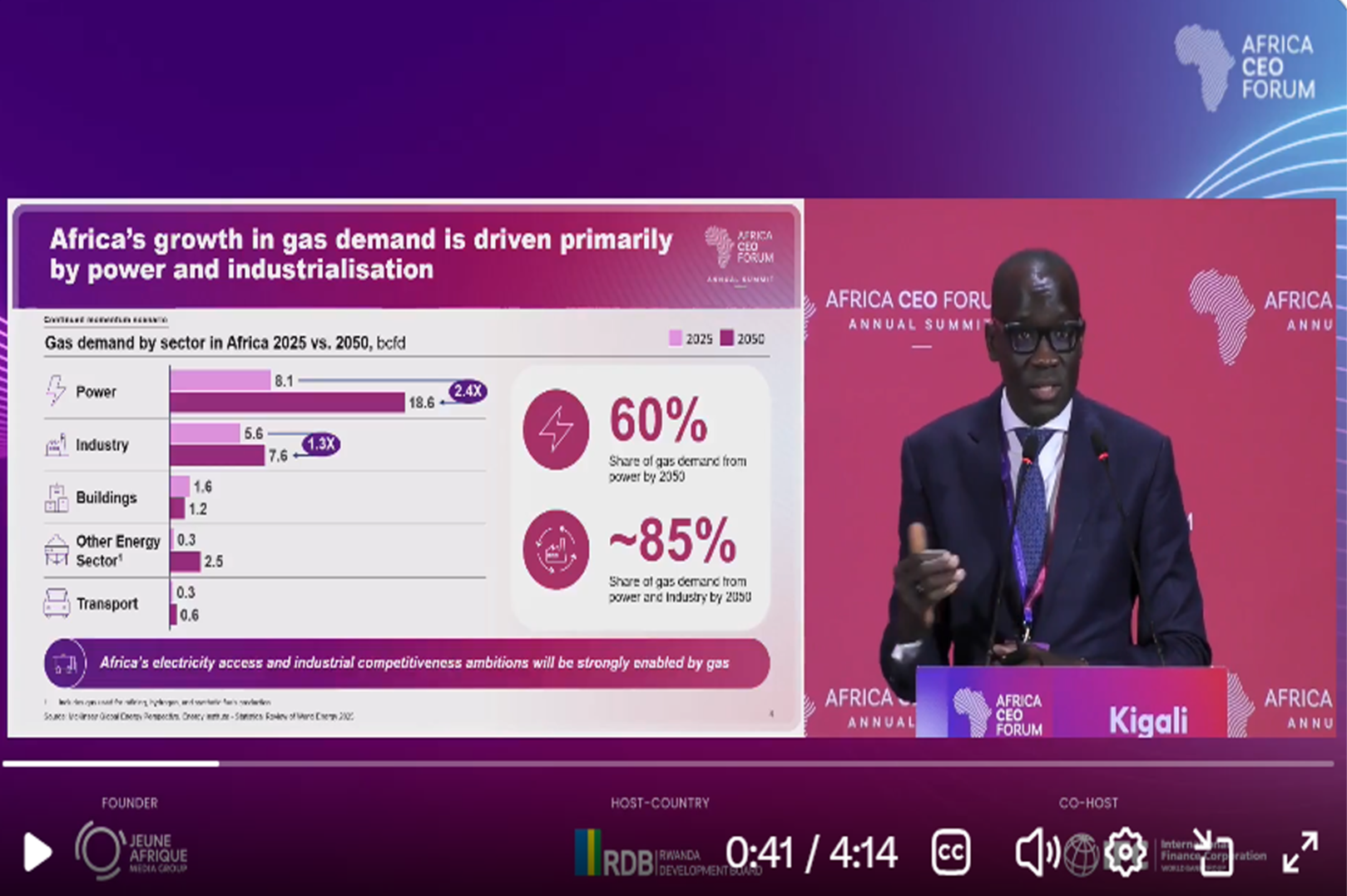

This contradiction framed the opening diagnosis delivered by Acha Leke, Chairman of McKinsey Africa, on the main stage of the annual Africa CEO Forum in Kigali.

Africa is the fastest-growing gas demand region in the world, expanding five times faster than the global average, with power generation and industry alone accounting for 85% of this demand. Seven countries concentrate 90% of the continent’s reserves. The resource is abundant, demand is rising, but the infrastructure needed to connect supply and consumption simply does not exist at a continental scale.

Today, 34% of African gas is directed toward export markets, mainly as LNG shipped to Europe where prices are higher and buyers more reliable. The remaining 63% of domestic consumption appears reassuring until one realizes it is concentrated in just four countries: Algeria, Nigeria, Egypt, and Libya. Looking at the continent’s pipeline map, the conclusion is clear: Africa’s gas infrastructure was designed to leave the continent, not circulate within it.

Leke’s prescription aligns with the “New Deal” the Forum has been advancing since its inception. It calls for credible energy off-takers, blended capital involving development finance institutions, national development banks, governments, and private investors, regulatory harmonization under the AfCFTA framework, and political commitment to long-term cross-border infrastructure. Without this combined push, production costs already 25% above the global average will continue to tilt economics toward exports.

The question repeatedly raised in Kigali remains unavoidable: who will power Africa, with African gas, for African industries and under what conditions?